《1 Introduction》

1 Introduction

Since the beginning of the 21st century, extreme weather and natural disasters closely related to global climate change have occurred frequently. Countries worldwide have set climate goals of reaching peak carbon emissions and achieving carbon neutrality, accelerating the clean and low-carbon energy transformations, and actively responding to climate change as a global issue [1–3]. China announced and promoted the implementation of the goals of reaching peak carbon and achieving carbon neutrality [4,5], which are not only a major contribution to the realization of the community of human destiny, but also reflect determination and responsibility for advancing the green and low-carbon transformations worldwide. Energy activities are the main sources of CO2 emissions in China; they account for approximately 87% of the CO2 emissions of the entire society and 73% of all greenhouse gas emissions. In particular, the power sector is important for carbon emissions, accounting for approximately 40% of energy carbon emissions, or approximately 4 × 109 t. The electrification of end-use energy consumption can be improved by replacing the direct use of fossil fuels such as coal, oil, and natural gas with electrical energy [6], which can significantly reduce the direct carbon emissions of end-use energy-using departments. Electricity is central to the energy transformation and a key field for carbon emission reduction [7–10]. The power sector will play a greater role in emission reduction and accelerate the construction of new electric power systems based on new energy sources [11]. Thus, it will promote the low-carbon transformation and the development of energy and electricity and make important contributions to the realization of China’s carbon neutrality goal.

The low-carbon transformation of energy and power is highly important for achieving the goals of reaching peak carbon emissions and carbon neutrality [12]. Research institutions worldwide have greatly advanced research on global low-carbon energy transformation paths. For example, the International Energy Agency and the International Renewable Energy Agency publish the Annual Development Report on World Energy [13,14] and have developed various comprehensive energy-economy models such as the MARKEL-MACRO, TIMES, and C-REM models, which provide guidance and tools to support research on decarbonization transformation paths for society as a whole and various sectors, with the goal of carbon neutrality. Domestic universities and research institutes [15–17] have conducted multi-scenario analyses of China’s low-carbon transformations of the energy and power sectors with the goals of reaching peak carbon emissions and achieving carbon neutrality by establishing scenarios for policy, stronger emission reductions, and limiting the global temperature increase to 2 °C or 1.5 °C. Note that China’s carbon emission peak, plateau period, and transformation path will be completely different from the long emission reduction path of major developed countries after a natural peak [18,19]. The low-carbon transformation of the power sector will inevitably face comprehensive challenges in areas including planning, policy, technology, industry, and economy. Systematic and in-depth research in multiple directions such as safety, economy, and environmental friendliness should be conducted to address multi-objective trade-offs and overall optimization events in various uncertain internal and external environments. Examples include the coordination of the emission reduction responsibilities and processes of the power industry and other industries across society. Such research should consider the impacts of key new technologies such as new types of power storage, carbon capture, utilization, and storage (CCUS), and hydrogen energy in the low-carbon transformation of the power industry [20–22]; a reasonable approach to the development of coal-fired power; the scientific development and utilization of new energy sources; and the challenge of power balance.

In this work, the quantitative reduction of carbon emissions by China’s power industry was taken as the main constraint. This constraint was considered in the context of key boundary conditions such as economic development, energy and power demand, and resources and the environment, and three low-carbon transformation scenarios for the power industry were developed: deep low-carbon, zero-carbon, and negative-carbon scenarios. The optimized power supply structure configuration, carbon emission reduction, and power supply cost under each scenario were compared and analyzed, and urgent problems in path implementation were identified to provide a basic reference for the power transformation and medium- and long-term development research with the goals of reaching peak carbon emissions and achieving carbon neutrality.

《2 Method of multi-scenario analysis of power transformation with the goal of reaching peak carbon emissions and achieving carbon neutrality》

2 Method of multi-scenario analysis of power transformation with the goal of reaching peak carbon emissions and achieving carbon neutrality

《2.1 Research models and methods》

2.1 Research models and methods

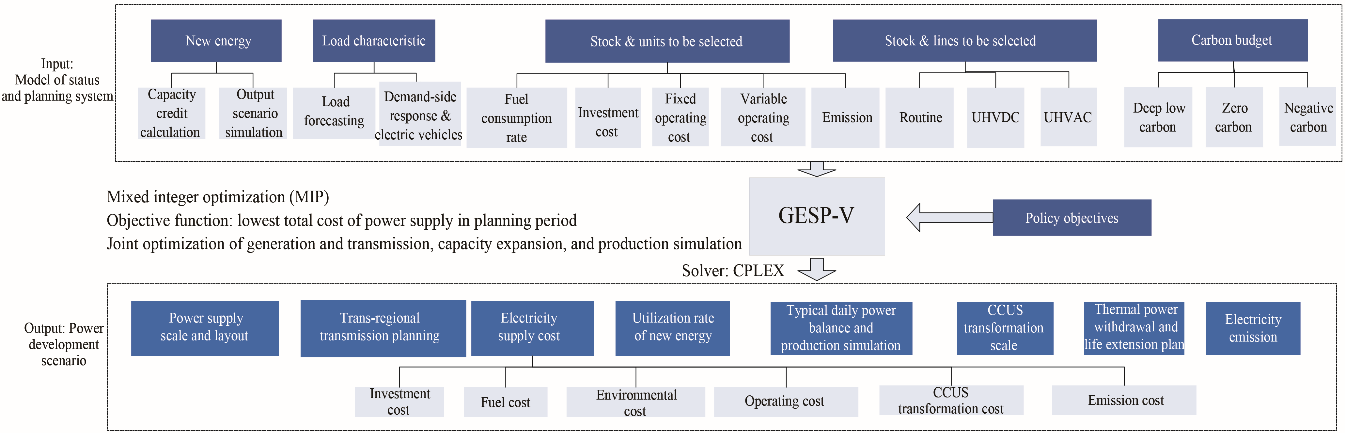

Quantitative and qualitative methods were used to meet the following research objectives. (1) Evaluate the carbon budget of the power system. The total budget of carbon emissions from China’s power sector from 2020 to 2060 was determined. This budget was constrained by the goals of reaching peak carbon emissions and achieving carbon neutrality in the context of current economic and social development. The current status of international carbon emission reduction, the development trends of different industries, and the difficulty of carbon emission reduction were considered. (2) Define transformation scenarios and key boundary conditions. Three scenarios for the transformation and development of the power system were developed: deep low-carbon, zero-carbon, and negative-carbon scenarios. Differences in the responsibility for reducing carbon emission and the implementation of key measures in the power system were considered, along with key boundary conditions and parameters such as national economic growth, energy and power demand, macro-policy objectives, energy resource potential, and technical economy. (3) Optimize the transformation path of the reduction of carbon emissions by the power sector (Fig. 1). For each development scenario, GESP-V, a software package for power planning to reach peak carbon emissions and achieve carbon neutrality, was used to optimize the transformation path of the power structure, emission reduction path, and power supply cost. GESP-V was independently developed by State Grid Energy Research Institute Co., Ltd., and used a multiregional power planning model with new energy as its core. It can reflect the impacts of key technologies and concepts such as power balance, carbon emission constraints, carbon capture methods, hydrogen production by electricity, and new energy utilization. System tools such as integrated power planning, production simulation, and policy analysis can be used to optimize and analyze the energy and power development path, power development scale configuration, power flow scale, capture scale after the CCUS transformation of conventional power supplies, and reduction in carbon emissions from the power sector under various scenarios. (4) Analyze key problems and suggest coping strategies (Fig. 2). The path optimization results for each development scenario were compared. Then key issues such as the approach to coal-fired power, new energy development and utilization, diversification of the clean energy supply, and power balance were considered, and technical, economic, industrial, and policy suggestions for the low-carbon transformation were formulated.

《Fig. 1》

Fig. 1. Optimization model of low-carbon transformation of power sector to reach peak carbon emissions and achieve carbon neutrality.

Note: UHVDC: ultrahigh-voltage direct current transmission; UHVAC: ultrahigh-voltage alternating current transmission.

《Fig. 2》

Fig. 2. Research framework of low-carbon transformation of power sector to reach carbon peak and achieve carbon neutrality.

《2.2 Carbon budget of electricity》

2.2 Carbon budget of electricity

The carbon budget is the upper limit of cumulative CO2 emissions required to control global surface temperature within a given range in a specific period. The maximum global temperature increase has an approximately linear relationship with cumulative CO2 emissions, and the carbon climate response (CCR) index can be used measure this approximately linear relationship [23, 24].

where ΔT is the global temperature increase over a period of time, and ET is the cumulative CO2 emissions over this period. The CCR index is usually 1.0–2.1 ℃/(1012 t CO2).

According to the calculations of the Intergovernmental Panel on Climate Change [25, 26], the remaining carbon budget to limit the global temperature rise to 2 ℃ is 1.2 ×1012–1.5 ×1012 t CO2, and that to limit it to 1.5 ℃ is 4.2 × 1011–5.8×1011 t CO2. To rationally allocate the international global carbon budget, research institutions in various countries are exploring methods of allocating carbon emission limits. Although a unified allocation scheme for carbon emission rights has not yet been established, two typical allocation concepts based on per capita carbon emissions and cumulative per capita carbon emissions have been proposed. In China, to break down the national carbon budget according to industry, it is necessary to consider the carbon emission status, carbon emission reduction difficulty, carbon emission reduction potential and technology, and economic differences between industries across society. This study comprehensively considered international carbon emission schemes, current carbon emissions, and differences in emission reduction capacity among domestic industries on the basis of the global residual carbon budget. The predicted carbon emission budget of China’s power system from 2020 to 2060 is 7.8 ×1010–1.3 ×1011 t CO2.

《2.3 Development scenarios and key boundary conditions》

2.3 Development scenarios and key boundary conditions

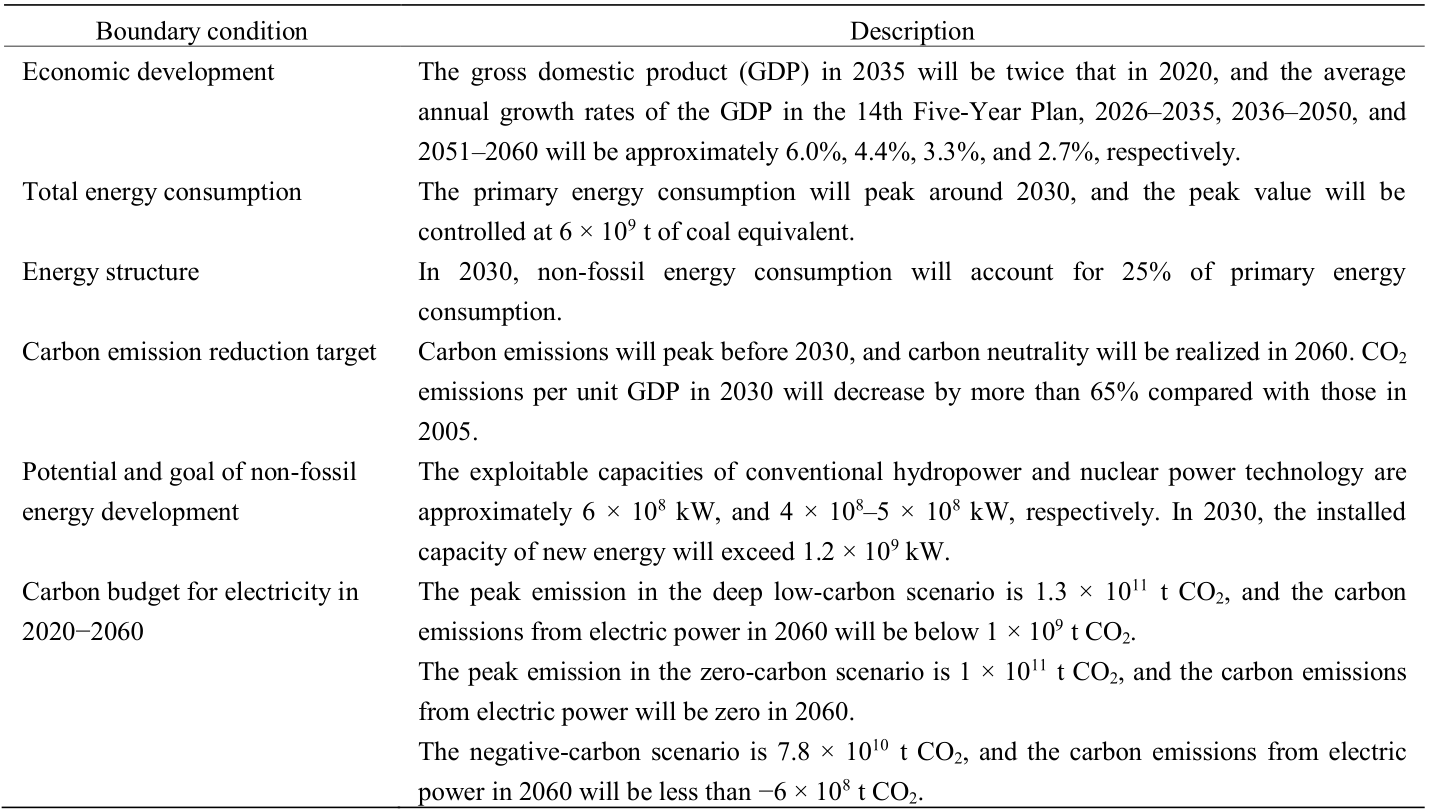

Deep low-carbon, zero-carbon, and negative-carbon scenarios for the transformation of the power system were established taking 2060 as the target year (Table 1). Different responsibilities for the reduction of carbon emissions within the power system and the implementation of key measures for emission reduction were considered. Important problems with each path to carbon neutrality were analyzed, and the feasibility and challenges of various development paths were considered.

《Table 1》

Table 1. Scenarios for low-carbon power transformation.

2.3.1 Predicted power demand

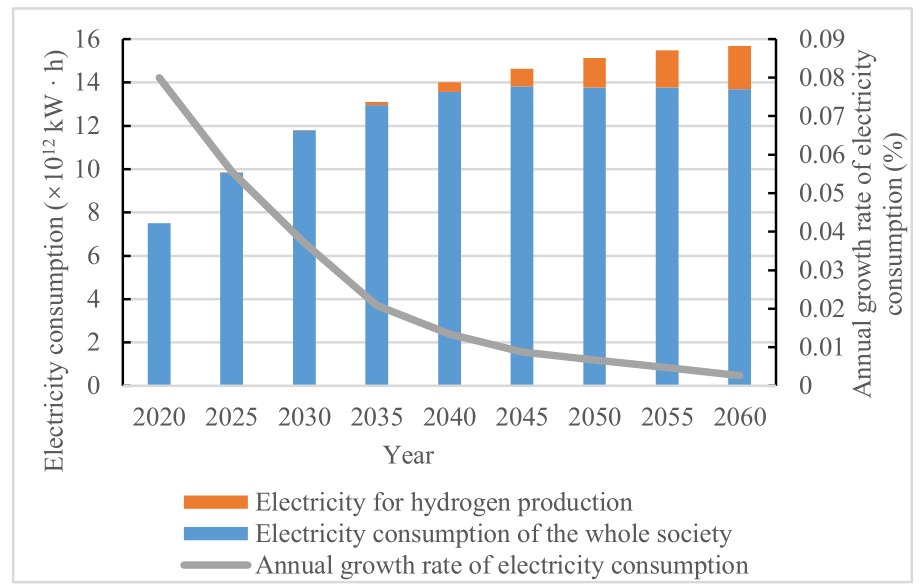

Considering factors such as economic growth, industrial structure adjustment, energy conservation and electric energy substitution, and hydrogen production by electricity, there is still considerable room for future growth in China’s electricity demand (Fig. 3). Total electricity consumption will be approximately 1.18 ×1013 kW·h in 2030, and the growth of electricity demand will tend to be saturated in 2040–2045 (that is, the average annual growth rate will become less than 1%). Total electricity consumption in 2060 will be approximately 1.57 ×1013 kW·h. In the long term, the proportion of hydrogen production from renewable energy sources will continue to increase, reaching approximately 1.7 ×1012 kW·h in 2060.

《Fig. 3》

Fig. 3. Predicted electricity consumption of entire society from 2020 to 2060.

2.3.2 Other key boundary conditions

In addition to the effects of power demand, the optimization of the low-carbon transformation of the power sector is also constrained by key boundary conditions (Table 2). These constraints include economic development goals, energy demand, the proportion of the energy structure contributed by non-fossil sources, non-fossil energy development potential and goals, key targets for carbon emission reduction, and the power carbon budget.

《Table 2》

Table 2. Other key boundary conditions for optimization of low-carbon transformation of power sector.

《3 Path for low-carbon transformation of power system》

3 Path for low-carbon transformation of power system

To optimize the path for the low-carbon transformation with the goal of reaching peak carbon emissions and achieving carbon neutrality, this study aimed to minimize the power supply cost from 2020 to 2060. The optimization variables were installed capacity for all types of power, power generation, and CCUS transformation scale, and constraints such as power balance, the carbon budget, and power generation from renewable energy resources were taken into account. A multi-scenario optimization planning model of the power system was then established, and the carbon emission reduction path and changes in power supply cost in each scenario were optimized.

《3.1 Transformation path of power supply structure》

3.1 Transformation path of power supply structure

The overall path of the power supply transformation shows a trend of continuous development of a clean power supply structure. The proportion of installed capacity and power generation from non-fossil energy has steadily increased, and new electric power systems based on new energy sources have gradually been developed.

(1) The installed power supply under the zero-carbon scenario is shown in Fig. 4. The total installed capacity of the power system will reach 4 ×109 kW in 2030, and the proportion of installed capacity for non-fossil energy will increase from 46% in 2020 to 64%. In 2060, the total installed capacity will reach 7.1 ×109 kW, and the proportion of installed capacity for non-fossil energy will increase to 89%. (2) The power generation structure under the zero-carbon scenario is shown in Fig. 5. Total power generation will reach 1.18 ×1013 kW·h in 2030, and the proportion of non-fossil energy power generation will increase from 36% in 2020 to 51%. In 2060, total power generation will reach 1.57 ×1013 kW·h; the proportion of non-fossil energy power generation will increase to 92%, and the proportion of coal-fired power will decrease to 4%.

《Fig. 4》

Fig. 4. Installed power supply from 2020 to 2060 under zero-carbon scenario.

《Fig. 5》

Fig. 5. Power generation structure from 2020 to 2060 under zero-carbon scenario.

In the deep low-carbon and negative-carbon scenarios, the installed capacity of non-fossil energy will account for 85% and 92%, respectively, in 2060, and power generation by non-fossil energy will account for 88% and 94%, respectively, in 2060.

《3.2 Path for carbon emission reduction in power system》

3.2 Path for carbon emission reduction in power system

The reduction of carbon emissions by the power sector occurs in three main stages: carbon peak, deep low-carbon stage, and carbon neutrality. The characteristics of each stage are as follows.

In the carbon peak stage under the zero-carbon scenario, the carbon emissions of the power system reach a peak around 2028, with a peak value of approximately 4.4 ×109 t CO2 (excluding carbon emissions from heating). This value accounts for approximately 49% of the peak CO2 emissions from energy combustion, of which coal-fired power emissions are approximately 4 ×109 t CO2, and gas-fired power emissions are approximately 4 ×108 t CO2. The power industry must bear the transfer of carbon emissions due to electrification in other industries. In addition, it will be difficult for non-fossil power generation to meet the new electricity demand in the carbon peak stage. These two factors may cause the peak carbon emissions of the power sector to lag behind those of other industries; overall, however, they can help the entire society to reach peak carbon emissions earlier. In the negative-carbon scenario, the power sector will assume more responsibility for reducing carbon emissions. It is estimated that carbon emissions will peak around 2025, two to three years ahead of the zero-carbon scenario, and the peak value will decrease to 4.1 ×109 t CO2. In the deep low-carbon scenario, it is predicted that carbon emissions from power will reach a peak at the end of the 15th Five-Year Plan period, and the peak value will increase to approximately 4.7 ×109 t CO2.

In the deep low-carbon stage, power emissions will peak and then enter a short plateau period (2–3 years). The overall carbon emission reduction rate will then decrease, slowly at first and then rapidly. With further improvements in the economy of new energy and energy storage technologies and greater commercial application of next-generation CCUS technology, the power system will enter the deep low-carbon stage. In the zero-carbon scenario, the carbon emissions from electric power will be reduced to less than 1 ×109 t CO2 in 2050.

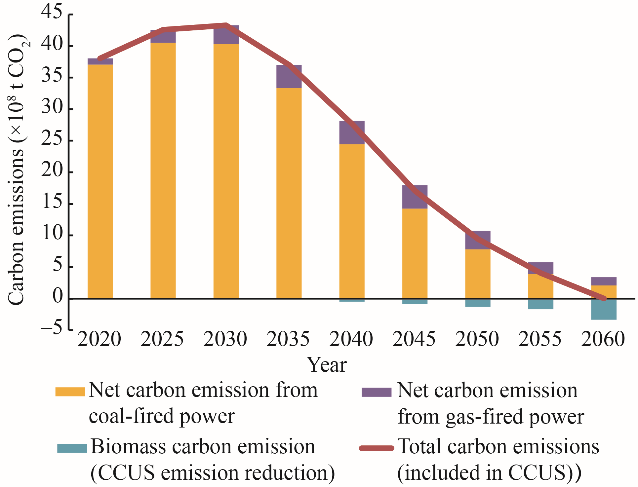

In the carbon-neutral stage, the power system will achieve zero carbon in 2060 (Fig. 6). In the zero-carbon scenario, the carbon emissions from coal-fired and gas-fired power are 5.3 ×108 t and 2.5 ×108 t CO2, respectively (excluding CCUS carbon capture). In addition, the CCUS carbon capture for coal-fired power, gas-fired power, and biomass power generation are 3.2 ×108 t, 1.2 ×108 t, and 3.4 ×108 t CO2, respectively.

《Fig. 6》

Fig. 6. Carbon emission and absorption of electric power from 2020 to 2060 under zero-carbon scenario.

《3.3 Cost analysis of power supply》

3.3 Cost analysis of power supply

The investment cost, operating cost, and carbon emission environmental cost structure in the planning cycle for the low-carbon transformation of the power system were estimated for each scenario (Fig. 7) on the basis of the installed power supply structure, generating capacity structure, and CCUS transformation of thermal power units. Different carbon emission reduction paths have different demands for low-carbon technologies and non-fossil energy, and there is an obvious positive correlation between power transformation costs and efforts toward emissions reduction. Under the zero-carbon scenario, considering a discount rate of 4%, the power supply cost in the entire planning cycle from 2020 to 2060 will be discounted to approximately 60 trillion CNY in 2020. New investment in power infrastructure accounts for the largest proportion (approximately 42%) of this cost. The grid-connected proportion of new energy in the negative-carbon scenario will increase rapidly compared with that in the zero-carbon scenario. The investment in flexible resources, transmission and distribution networks, and carbon capture and utilization equipment will also increase greatly, and the power supply cost will increase by approximately 17%. The deep low-carbon scenario has the lowest power supply cost, which is approximately 12% lower than that in the zero-carbon scenario.

《Fig. 7》

Fig. 7. Power supply cost and composition under each scenario.

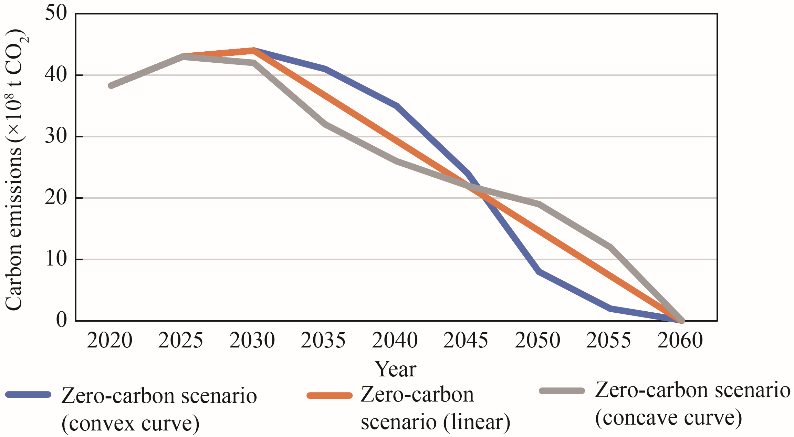

A comparison of different paths for the reduction of carbon emissions under the zero-carbon scenario (Fig. 8) reveals that for a given carbon budget scenario, the technical and economic performance of the “convex curve” emission reduction path, with initially slow reduction that becomes more rapid, is better. If the carbon emission reduction path for the power section maintains a uniform trend of a downward slope or downward concave curve, the requirements for the scale of new energy and the application of decarburization technology will be higher. It is estimated that the cost of power will increase by 4%–8% from 2020 to 2060. Therefore, the formulation of the carbon peak and carbon neutrality paths should take into account objective factors such as economic and social development trends and the maturity of key technologies. In addition, these paths should rationally allocate the responsibility for carbon emission reduction in different historical periods, avoid false starts and superficial carbon reduction, and be as practical and feasible as possible.

《Fig. 8》

Fig. 8. Comparison of paths for carbon emission reduction under zero-carbon scenario.

The calculated data show that the power supply cost fluctuates; it increases in the near and medium term, enters a plateau period, and then gradually decreases in the medium and long term. Under the zero-carbon scenario, to meet new electricity demand and achieve the goals of reaching peak carbon emissions and achieving carbon neutrality, all types of resources, especially new energy, must be rapidly developed. Thus, the corresponding investment will remain at a high level. When the penetration rate of new energy power generation exceeds 15%, the system cost reaches the critical point of rapid growth. The estimated system costs in 2025 and 2030 are 2.3 and 3 times that in 2020, respectively. These factors will enhance the fluctuation of power supply costs. It is estimated that the power supply costs in 2020–2025, 2025–2030, and 2030–2040 will be approximately 14.5 trillion CNY, 6.1 trillion CNY, and 33.0 trillion CNY, respectively (excluding discounts). Around 2045, the power supply cost will enter a plateau period; electricity demand will grow more slowly, and the less investment in new power infrastructure will be needed. Electricity demand will be met mainly by new energy power generation with a low grid-connected marginal cost, and the system operation cost will enter a plateau period.

《4 Major problems urgently requiring solutions to realize the low-carbon transformation of the power system》

4 Major problems urgently requiring solutions to realize the low-carbon transformation of the power system

During the transformation to low-carbon power, new energy, represented by wind energy and photovoltaics, will become the main power supply, resulting in strategic changes to the existing power system as a whole [27]. On the supply side, new energy will gradually account for most of the installed capacity and electricity supply. On the user side, a large number of modes that integrate power generation and consumption, such as distributed power generation and multi-load and energy storage, will emerge. Regarding power grids, a pattern will gradually emerge in which large power grids predominate, and various types of power grid will coexist. The operating mechanism of power systems will inevitably undergo profound changes. To realize the development goals of reaching peak carbon emissions and achieving carbon neutrality in China, it is necessary to focus on the following four issues.

《4.1 Identification of a scientific approach to coal-fired power development》

4.1 Identification of a scientific approach to coal-fired power development

Coal-fired power and non-fossil energy are not in a simple trade-off relationship, but should be in a coordinated and complementary development relationship. Solving the problem of coal-fired power development is the key to steadily realizing the low-carbon transformation of the power system in China. Coal-fired power should shift from the main source of electricity to the main type of capacity, which will not only open space for the development of new energy, but also provide flexibility to ensure the safety of the energy supply. The installed capacity of coal-fired power in China is approximately 1.08 × 109 kW, of which approximately 9 × 108 kW consists of high-parameter and large-capacity coal-fired power units. Measures should be taken to rationally use these high-quality stock assets, scientifically plan an exit path for coal-fired power units, and coordinate the development of coal-fired power and renewable energy so that the power supply remains safe and stable without disruption by a large-scale rapid decrease in coal-fired power.

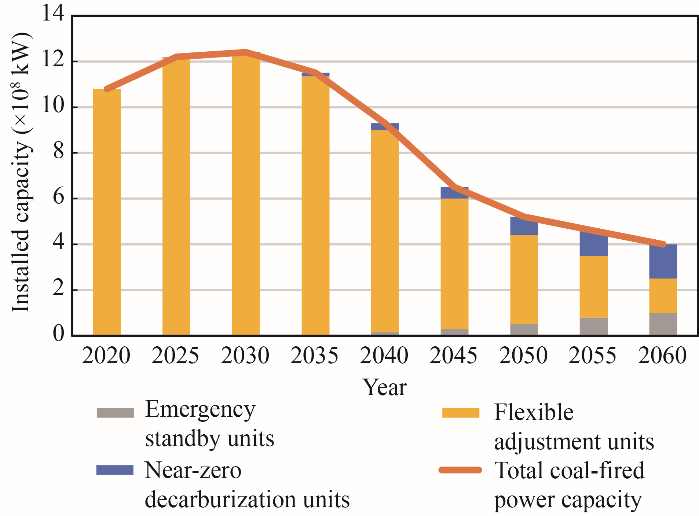

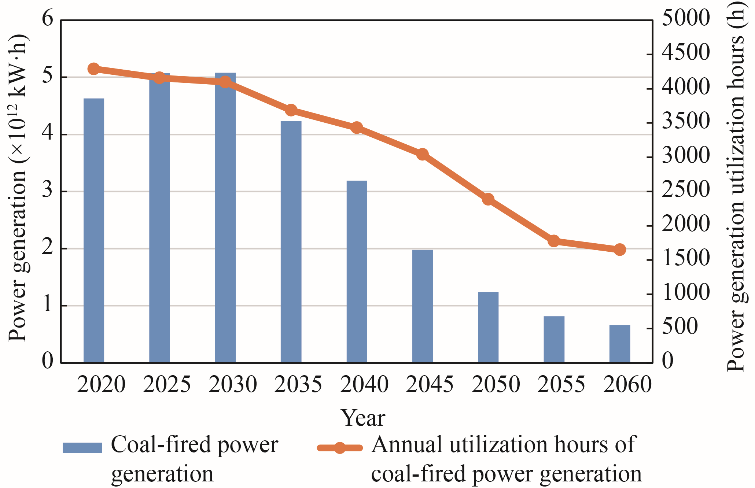

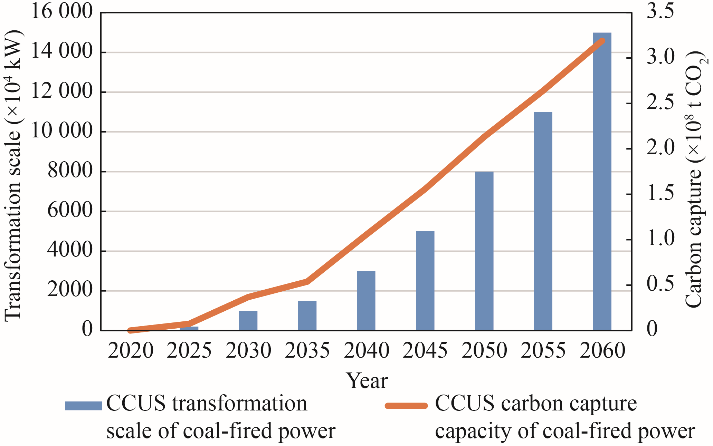

The development path of coal-fired power should follow three stages: increased capacity and controlled quantity, controlled capacity and reduced quantity, and reduced capacity and quantity (Figs. 9–11). During the 14th Five-Year Plan period, it is difficult to halt the development of coal-fired power, and the installed capacity still needs to increase to a certain extent. Therefore, during the first stage, it is necessary to strictly control the growth of power generation. The peak installed capacity is approximately 1.25 × 109 kW, and the peak power generation is approximately 5.1 × 1012 kW·h; the latter will occur two or three years before the former. Newly added coal-fired power provides mainly peak power balancing and emergency support and ensures the safe, stable operation of the power system. During the 15th Five-Year Plan period, coal-fired power will enter a plateau period at the peak installed capacity, and power generation and coal consumption will decrease steadily. Coal-fired plants will take on additional functions such as system regulation and peak power balancing. It is estimated that in 2030, coal-fired power generation will reach 5 × 1012 kW·h, which is 1 × 109 kW·h below the peak value, and the utilization hours of coal-fired power generation will be reduced to less than 4000 h. During the 15th Five-Year Plan period, the CCUS transformation of the coal-fired power industry will enter an initial stage in which applications are demonstrated and industrialization is promoted. In 2025 and 2030, the cumulative transformation scale will be 2 ×106 kW and 1 ×107 kW, and the carbon capture scale will be 8 ×106 and 3.7×107 t/a, respectively. After 2030, the installed capacity and power generation of coal-fired power will decrease steadily, and some plants will gradually withdraw from routine operation and serve as emergency standby. In the long run, CCUS equipment will be installed, the use of near-zero decarburization units will gradually increase, and a new development model of a carbon circular economy will be established. In 2060, the installed coal-fired power capacity will decrease to 4 ×108 kW, which will account for only 5.6% of power generation.

《Fig. 9》

Fig. 9. Installed capacity of various types of coal-fired power facilities from 2020 to 2060 under zero-carbon scenario.

《Fig. 10》

Fig. 10. Coal-fired power generation and utilization hours from 2020 to 2060 under zero-carbon scenario.

《Fig. 11》

Fig. 11. Carbon capture capacity and CCUS transformation scale of coal-fired power under zero-carbon scenario.

《4.2 Expansion of development model and diversification of new energy supply》

4.2 Expansion of development model and diversification of new energy supply

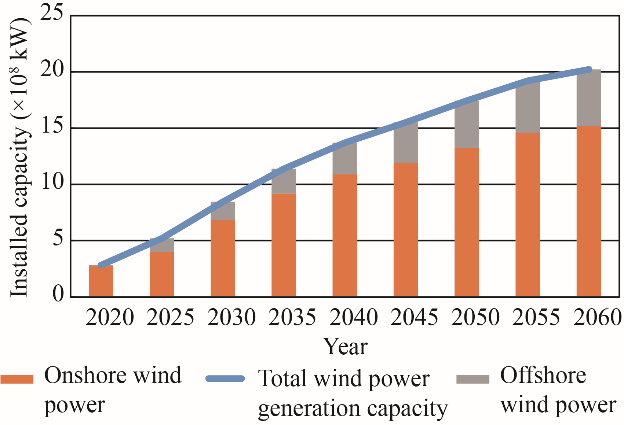

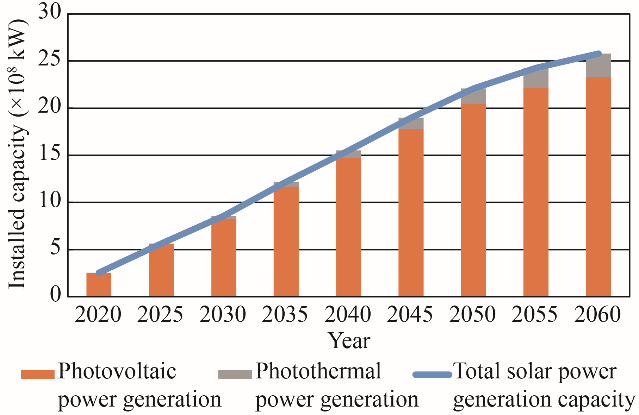

As new energy gradually becomes the main power supply, it is advisable to adhere to centralized and distributed development and optimize the configuration in stages. China is rich in new energy resources for power generation, and the technically and economically exploitable quantities of wind power and photovoltaic power are 3.5 × 109 kW and 5 × 109 kW, respectively. The costs are decreasing rapidly because of rapid technological progress and reasonable market competition. China’s new energy industry chain is relatively complete, and the annual production capacities of photovoltaic modules and wind turbines are 1.5 × 108 kW and 6 × 107 kW, respectively, ensuring large-scale, high-intensity, and sustainable development and utilization (Figs. 12 and 13).

《Fig. 12》

Fig. 12. Installed capacity of wind power generation from 2020 to 2060 under zero-carbon scenario.

《Fig. 13》

Fig. 13. Installed capacity of solar power generation from 2020 to 2060 under zero-carbon scenario.

Regarding wind power, decentralized and offshore wind power in the eastern and central regions should be developed according to local conditions in the near future. Local consumption should be prioritized, and the intensive development of wind power bases in the western and northern regions should be continually promoted. In the long run, when decentralized wind power resources are completely developed in the eastern and central regions, the focus of wind power development should return to the western and northern regions, and offshore wind power should be gradually expanded to far offshore. It is estimated that in 2060, the installed capacity of wind power will be 2 ×109 kW (including 5 ×108 kW of offshore wind power).

Regarding solar energy, photovoltaic power should remain the leading mode in the near future. The development of distributed photovoltaics in the eastern and central regions should be prioritized, whereas the construction of centralized bases of solar power generation should be promoted in the western and northern regions. In the medium and long term, the construction of solar power generation bases including photothermal power generation should continue to be expanded in Northwest China and possibly other areas. It is estimated that in 2060, the installed capacity for solar power generation will be 2.6 × 109 kW (including 2.5 × 108 kW of photothermal power generation).

Regarding medium- and long-term development, it is difficult to fully realize new energy utilization relying solely on the power system. Therefore, the development of a circular carbon economy across systems will be an important means of diversifying new energy utilization. It is advisable to use renewable energy sources to generate hydrogen, gas, and heat (power-to-X) and cross-energy system utilization modes and to combine them with CO2 capture by thermal power CCUS to produce methanol and methane (which can be used as industrial raw materials) to expand the scale of the carbon circular economy.

《4.3 Building a diversified clean energy supply system》

4.3 Building a diversified clean energy supply system

The approach to the development of various types of clean power sources is the focus of the low-carbon transformation of the power sector. It is unscientific to rely solely on the growth of new energy. To obtain overall balance and complementary functionality, it is necessary to clarify the approach to the development of various types of power sources, giving equal attention to the green and low-carbon transformations of energy and the flexibility needed to adjust resources to supplement shortcomings, thus realizing the coordinated development of various power sources such as water, nuclear, wind, and photovoltaics, as well as storage.

First, efforts should be made to promote hydropower development and the safe and orderly development of nuclear power. It is necessary to accelerate the development of high-quality hydropower sites in Southwest China before 2030 and focus on the promotion of hydropower development in the Tibet Autonomous Region after 2030. In 2030, the total installed hydropower capacity will exceed 4 × 108 kW; the annual power generation will be approximately 1.6 × 1012 kW·h, and the development rate (excluding Tibetan hydropower) will exceed 80%. Hydropower will be fully developed in 2040, and the installed capacity will remain above 5 ×108 kW in 2060. To ensure safety, nuclear power will be developed in an orderly manner. Before 2030, six to eight units will be launched annually, and the installed capacity of nuclear power will be approximately 1.2 ×108 kW in 2030. With the development of coastal station resources, inland nuclear power construction will be initiated in due course after 2030, and the installed capacity will increase to approximately 4 ×108 kW in 2060.

Second, the moderate development of gas-fired power should be pursued to enhance the flexibility of the power system and realize a diversified power supply. The emission per kilowatt hour of gas-fired power is approximately 50% of that of coal-fired power, and its capacity for flexible adjustment is excellent. Moderate development is a realistic choice to ensure the safety and stability of the electricity supply. Gas-fired power is used mainly for peak shaving, and it is estimated that the installed capacities in 2030 and 2060 will be 2.2 ×108 kW and 4 ×108 kW, respectively. In the future, it will still be necessary to consider the external dependence of natural gas, power generation cost, technology types, and other issues and to explore carbon cycle modes such as blending hydrogen with natural gas and producing natural gas from hydrogen and CO2 to serve as a supplementary gas source.

Third, it is necessary to rationally coordinate the development of pumped storage and new types of power storage. In the near and medium term, if station site resources meet the requirements, pumped storage should first be developed to ensure power balance and provide system inertia. High-quality station site resources should be exploited in the medium and long term. It is estimated that the installed capacity of pumped storage will reach 4 × 108 kW in 2060. To ensure power balance and new energy consumption, new types of power storage should be rapidly developed in the medium and long term. The installed capacity is expected to reach 2 ×108 kW in 2060.

《4.4 Solving the practical problems of power balance and supply security》

4.4 Solving the practical problems of power balance and supply security

Power balance is a major challenge in the low-carbon transformation of electricity that urgently requires solution. Because of recent coal shortages and obvious increases in coal prices, limited production and power have occurred in many places, causing great concern among all parties. Note that coal will still be a vital energy source in China for a certain period of time. To solve the problems of supply and demand, order, and price in the coal market, efforts should be made to build a diversified clean energy supply system and thus ensure an adequate power supply.

Coal-fired power is still the main power source ensuring power balance. The effective output of new energy sources is unstable and small (Fig. 14). It is estimated that new energy will contribute 6% and 7% in 2025 and 2030, respectively, whereas the contributions of coal-fired power will be as high as 57% and 48%, respectively. The full exploitation of demand-side resources is also crucial to ensure the safe operation of power systems and promote new energy consumption. It is estimated that available demand-side resources will exceed 6% and 15% of the maximum load in 2030 and 2060, respectively. Therefore, measures should be taken to establish and improve the demand-side resource utilization system in terms of planning and design, market cultivation, mechanism improvement, and infrastructure construction.

《Fig. 14》

Fig. 14. Contributions of various power sources in China from 2020 to 2060.

In the long run, ensuring power balance depends on diversified clean energy sources. It is estimated that the national demand for power balance capacity in 2060 will be 2.8 ×109–3.2 ×109 kW. The installed capacity of wind energy and photovoltaics is approximately 4.6 ×109 kW; however, the effective capacity available for power balancing is only approximately 4 ×108–5 ×109 kW, which is only approximately 15% of the demand. Clean energy sources such as hydropower, nuclear power, gas-fired power, and biomass contribute 40% to the power balance capacity; pumped storage and new types of power storage contribute 17%, and CCUS transformation, peak shaving, and emergency standby coal-fired power contribute 5%, 5%, and 3%, respectively.

In the long run, there are many paths for the development of the power supply in China, and they are highly uncertain. To mitigate the risks associated with the uncertainties, a more stable power supply system should be established to improve the security of the power supply in extreme circumstances. On the basis of the target constraints of reaching peak carbon emissions and achieving carbon neutrality, two scenarios (smooth reduction and accelerated reduction of the installed capacity of coal-fired power) were considered in simulations of the security of the power supply (Fig. 15). In the smooth reduction scenario, the installed capacity of coal-fired power in China will remain 8 ×108 kW in 2060, including 3.8 × 108 kW from near-zero decarburization units, 2.2 × 108 kW from flexible regulation units, and 2 × 108 kW from emergency standby units. After 2030, the installed capacity of coal-fired power will be smoothly decreased by life expansion and replacement of retired units with newly built units. At the same time, the amount of emergency standby coal-fired power that is retired without being dismantled will increase. The installed capacity of new energy to be configured is 3.9 ×109 kW. In the accelerated reduction scenario, 4 ×108 kW of installed capacity of coal-fired power will be reserved in China in 2060, including 1.5 × 108 kW from near-zero decarburization units, 1.5 × 108 kW from flexible regulation units, and 1×108 kW from emergency standby units. After 2030, the natural decommissioning of coal-fired power equipment will rapidly accelerate, and small-scale life extension and decommissioning of replacement units will be performed. The installed capacity of new energy to be configured will be 4.6 × 109 kW.

《Fig. 15》

Fig. 15. Comparison of coal-fired power reduction scenarios in China from 2020 to 2060.

The power supply will be significantly more stable during extreme weather such as windless, cloudy, rainy, and freezing periods under the smooth reduction scenario than under the accelerated scenario. However, the redundant reserve cost of the system will increase greatly under smooth reduction. In addition, the CCUS transformation will be needed earlier; the numbers will increase (for example, a carbon capture capacity of 1.4 ×109 t will be needed in 2060), and the power supply cost in the entire planning period will increase by approximately 4%.

《5 Countermeasures and suggestions》

5 Countermeasures and suggestions

《5.1 Optimizing top-level design of power industry to plan for steady progress on power transformation》

5.1 Optimizing top-level design of power industry to plan for steady progress on power transformation

Efforts should be made to determine the carbon emission reduction budgets of all provinces and industries, in particular to clarify the carbon budget of the power industry and to scientifically formulate and implement the peak times and main indicators of carbon emissions. To accelerate the development of non-fossil energy sources such as new energy, hydropower, and nuclear power, it is necessary to comprehensively consider the need for power supply security and the flexible adjustment of system resources and to coordinate the scale and timing of coal-fired power withdrawal and the development of renewable energy. In addition, measures such as prolonging the life of coal-fired power plants and converting retired coal-fired power plants into emergency standby units should be taken to avoid threats to the safety and stability of the power supply resulting from the large-scale rapid withdrawal of thermal power. Attention should be given to changes in the internal and external environments, for example, in the carbon budget, industrial structure, technology and policy, and the path and timing of the low-carbon transformation of the power sector.

《5.2 Performing core scientific and technological research on green and low-carbon power and coordinating the technical and industrial configuration of the entire power chain》

5.2 Performing core scientific and technological research on green and low-carbon power and coordinating the technical and industrial configuration of the entire power chain

Measures should be taken to strengthen the guidance of the national science and technology strategy, demonstrate and formulate the scientific and technological development of a new type of power system, prepare a roadmap for the development of carbon-neutral technology in the power industry, and develop targeted plans for major breakthroughs. It is recommended that national laboratories and innovation platforms be developed around a new type of power system and that a number of major technical projects be supported by national science and technology plans. In addition, breakthroughs in the following are urgently needed: new clean energy power generation; the planning, operation, safety, and stability control of a new type of power system; a new advanced transmission system; new types of power storage; and the coordinated utilization of electricity, hydrogen, and carbon. Moreover, it is essential to increase research and development, the demonstration and large-scale application of advanced and applicable technologies, and the construction of a system for technological and industrial innovation involving government, industry, universities, and research institutions that is deeply integrated with the construction of a new type of power system. It is also recommended that the research and development of key technologies and demonstration projects for carbon neutrality be supported, that the scientific and technological policy system be better supported, and that the high-quality and sustainable development of the power industry be promoted.

《5.3 Improving the coordination of a market mechanism featuring balanced interests and establishing a guarantee system for green financial policy》

5.3 Improving the coordination of a market mechanism featuring balanced interests and establishing a guarantee system for green financial policy

It is necessary to give the market full play in its decisive role in resource allocation and adopt marketization-oriented means to reduce the utilization costs of new energy systems. A capacity compensation mechanism should be explored; the flexible resource allocation potential of source network load storage in the power system should be exploited, and the efficient use of new energy and the reliability of the power supply for users should be ensured. The market-oriented mechanism for establishing the prices of electricity and other types of energy should be improved; the policies for differential, time-of-use, and residential ladder electricity pricing should be optimized, and industrial restructuring and the alleviation of the tight power supply should be promoted. A total carbon emission control target and quota allocation mode should be set scientifically; a linkage mechanism between carbon and electricity prices should be established, and carbon trading and other types of green trading should be coordinated. Government investment should be given full play in its guiding role, and an investment and financing policy system should be built that is consistent with the goals of reaching peak carbon emissions and achieving carbon neutrality. In addition, the orderly development of green and low-carbon financial products and services should be promoted, and monetary policy tools for the reduction of carbon emissions should be established. Finally, a green credit evaluation mechanism should be established, and the green financial policy framework should be improved.

京公网安备 11010502051620号

京公网安备 11010502051620号