2007, Volume 9, Issue 11

Strategic Study of CAE >> 2007, Volume 9, Issue 11

The Model for Loan Portfolio With Safety-first Criterion

1. Institute of Systems Engineering, Tianjin University, Tianjin 300072, China ;

2. Department of Computer Science, Dezhou University, Dezhou, Shandong 253023, China

Next Previous

Abstract

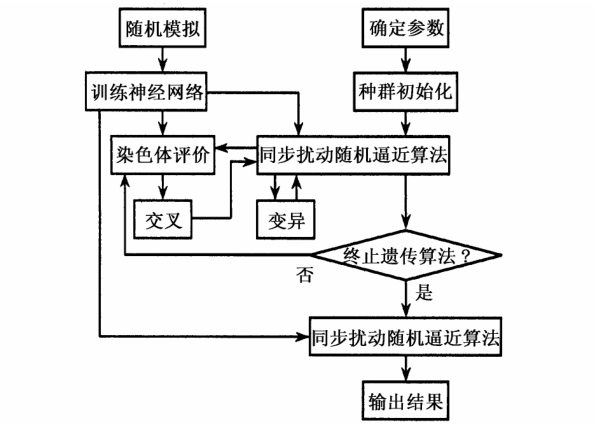

This paper proposes the model for loan portfolio under probability criterion, and designs the hybrid optimization algorithm based on random simulation to solve the model. The algorithm can solve the models with the return rates with any probability distributions, and is not subject to the assumption that the return rates have normal distributions. The feasibility of the algorithm is verified by two examples.

Keywords

loan portfolio ; safety-first criterion ; random simulation ; genetic algorithm(GA) ; simultaneousperturbation stochastic approximation(SPSA)

Figures

图1

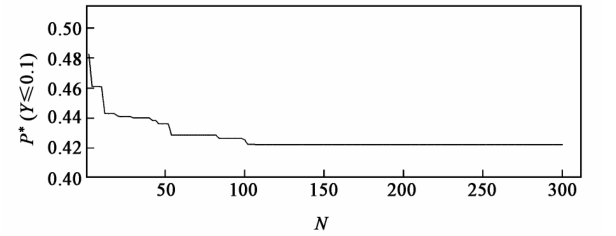

图2

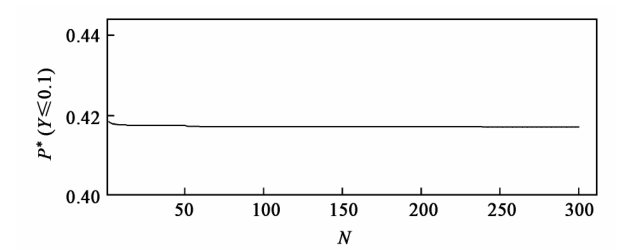

图3

References

[ 1 ] 韩其恒,唐万生,梁建峰.允许卖空情况下证券投资组合的概率准则模型[J].系统工程学报,2003,18(4):289~293 link1

[ 2 ] 梁建峰,唐万生.有交易费用的组合证券投资的概率准则模型[J].系统工程,2001,19(2):5~10 link1

[ 3 ] 马永开,唐小我.不允许卖空的多因素证券组合投资决策模型[J].系统工程理论与实践,2000,20(2):37~43 link1

[ 4 ] 荣喜民,张喜彬,张世英.组合证券投资模型研究[J].系统工程学报,1998,13(1):81~88 link1

[ 5 ] 唐小我,傅庚,曹长修.非负约束条件下组合证券投资决策方法研究[J].系统工程,1994,12(6):23~29 link1

[ 6 ] 王竹,唐小我,曹长修.加权行和指标下组合证券投资风险最小化迭代算法[J].系统工程,1994,12(5):53~58 link1

[ 7 ] Tang Wansheng , Han Qiheng , Li Guangquan . Cash Management decision with probability criterion [ A ] . Proceedings of IEEE International Conference on Systems , Man & Cybernetics[C] . AZ , USA : Tucson , 2001 . 2670 ~ 2673 link1

[ 8 ] Tang Wansheng ,Han Qiheng , Li Guangquan . The portfolio selection problems with chance-constrained [ A ] . Proceedings of IEEE International Conference on Systems , Man & Cybernetics[C] . AZ , USA : Tucson , 2001 . 2674 ~ 2679 link1

[ 9 ] Spall J C . Multivariate stochastic approximation using a simultaneous perturbation gradient approximation [ J ] . IEEE Transactions on Automatic Control , 1992 , 37 : 332 ~ 341 link1

[10] 刘宝碇,赵瑞清,王纲.不确定规划及应用[M].北京:清华大学出版社,2003

京公网安备 11010502051620号

京公网安备 11010502051620号